REVEALED: The 'best' banks for foreigners in Denmark

We asked our readers in Denmark to recommend the best banks for foreign residents in the Nordic country. Here’s what you had to say.

Setting up a new bank account is one of the many things one must consider when relocating to another country. Different banks can come with their own rules, requirements and hoops to jump through to open an account, whether it's on CPR (personal registration) number, MitID, mortgages or transactions.

READ ALSO: REVEALED: Danish banks’ policies on non-Danish speaking customers

But what are the best, or worst, banks in Denmark for international residents?

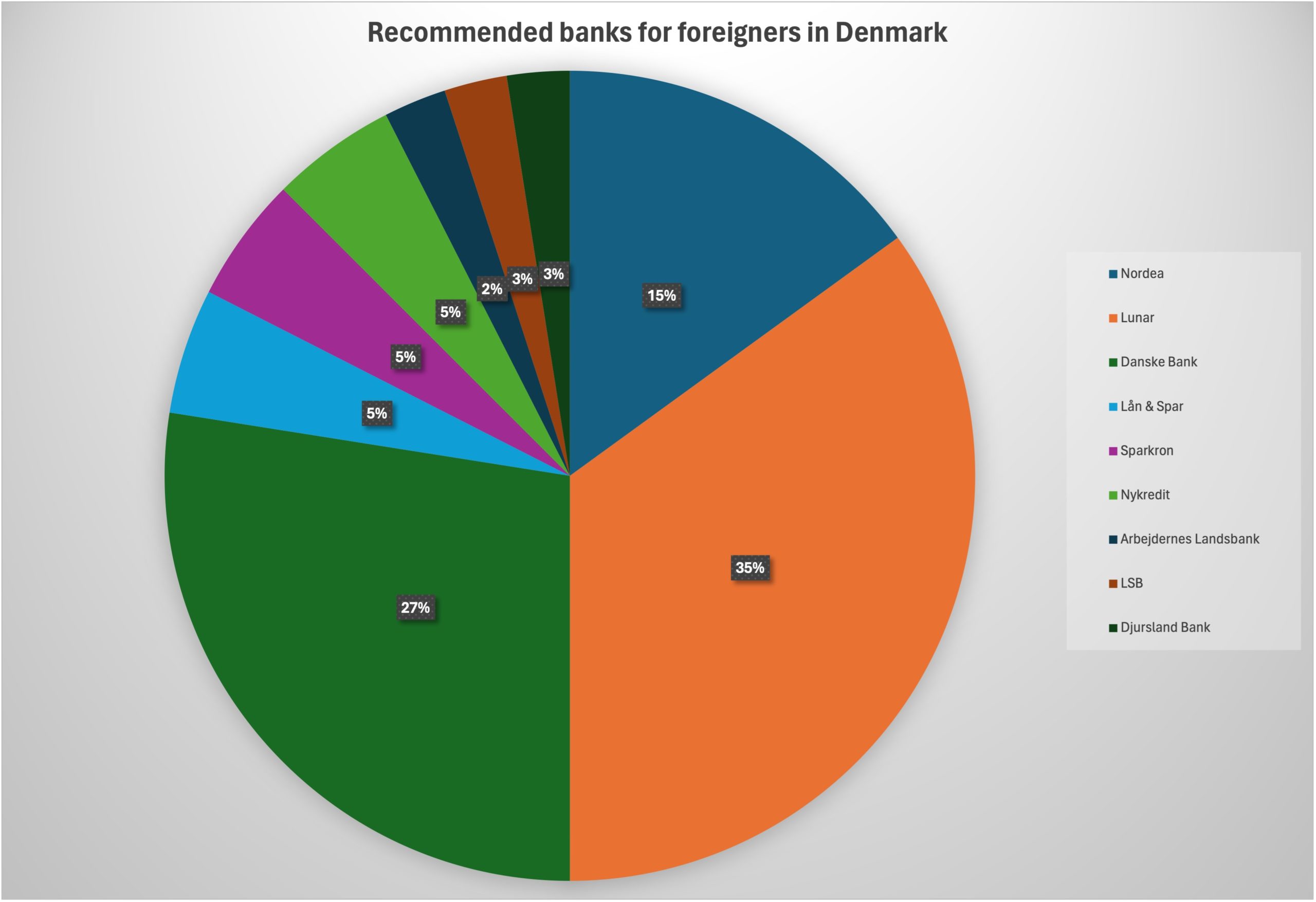

Of the responses we received to our survey, two banks stood out as being those readers are most likely to recommend. Lunar was recommended by 35 percent people and Danske Bank by 27 percent.

The third-most recommended bank was Nordea, while several other banks got one or two recommendations.

Why were these banks singled out for recommendation?

For Lunar, the ease and speed of opening an account, app in English, and lack of a conversion fee for foreign currency were cited as benefits of using the bank.

“Easiest to open an account and get set up. Their app is great. I have found out that the process for other banks to be quite time consuming and cumbersome,” one reader wrote.

“Easy to use and fully English friendly,” said a French reader in Copenhagen.

While Lunar is a 100 percent digital bank, the legacy bank Danske Bank, the largest lender in Denmark, was praised for similar reasons.

“Simple process and helpful customer care manager” were features at Danske Bank, one reader from India, who works for a large company in Copenhagen, wrote to say.

An English-language version of Danske Bank’s app and mobile banking, and the bank’s general use of English, were also cited by several readers.

“They have English web interface and happy to communicate in English,” one wrote.

READ ALSO: REVEALED: Danish banks’ policies on non-Danish speaking customers

Another said Danske Bank was “More open to our situation - was completely thrown out by Nordea when wanting make an account 5 years ago and, more recently, when I wanted to buy a house Nordea offered us laughable rates as foreigners.”

“Danske treated us as equals to citizens,” they said.

Despite this negative review of Nordea, the pan-Nordic bank also had its share of recommendations.

Nordea has “less fees, good service in English” one of our readers said, with another adding that it offers “excellent app in English, great customer service and easy home loan process for non-Danish speakers”.

There was also some praise for smaller banks. For example, Lån & Spar is “much more flexible when issuing loans for property purchases and are willing to go fairly close to the 5 percent minimum for down payments, whereas big banks will flat out reject you if you have less than 20 percent saved,” wrote Nikola from Bulgaria, who lives in Copenhagen.

“Additionally, their advisors are very responsive and skilful at explaining the complex Danish mortgage system,” he added.

Which banks should you avoid according to readers?

“Danske Bank, unless you're a Russian oligarch and need to launder some money,” according to Nikola, presumably in reference to a major money laundering scandal at Danske Bank in the late 2010s.

READ ALSO: Money laundering scandal costs trust amongst Danske Bank customers

“While they do cater to foreign customers, they clearly have a preference to very wealthy ones and will happily ignore everyone else,” Nikola elaborated.

The number of readers who advised against using a specific bank was limited, but the two banks most frequently mentioned were Danske Bank and Nordea. Since these two banks were also highly recommended, this may reflect their size.

One reader wrote that Nordea “really do not care for you”, with another saying “I started with Nordea but merely got a Dankort debit [card], no MasterCard and no benefits that's why I changed.”

READ ALSO: Dankort: What is Denmark’s payment card and how is it different from other card types?

It’s best not to use “tier 1 banks as Danske or Nordea as the onboarding could be very long due to which expats will not receive the account in time,” according to one reader, who may have had in mind the requirement for Danish salaries to be paid into a Danish bank account under immigration laws.

In general, avoid “all of those that don't have dedicated full-service English based web services”, said another of the readers who responded to our survey.

Any other advice?

“For everyday banking, there's very little difference from one bank to the next. They all have low fees and offer the basics. For mortgages, it's valuable to shop around and play them one vs the other, especially if you're a higher earner. Banks do have some leeway when it comes to loan fees and they'll be willing to go lower if they want to capture you as a customer,” Nikola said.

When you go to open an account, “have the documents like CPR number, residence permit , employment contract, passport, address proof from home country [and] rental agreement,” one reader said.

“Check for fees and go to the physical bank to get a feeling on how much the staff is willing to help you before you open an account,” another said.

They added that “I could feel Jyske [bank] was bad but had just arrived here so couldn’t see the difference yet between being a Dane [reserved towards strangers, ed.] and being annoyed [about helping] foreigners”.

Comments

See Also

Setting up a new bank account is one of the many things one must consider when relocating to another country. Different banks can come with their own rules, requirements and hoops to jump through to open an account, whether it's on CPR (personal registration) number, MitID, mortgages or transactions.

READ ALSO: REVEALED: Danish banks’ policies on non-Danish speaking customers

But what are the best, or worst, banks in Denmark for international residents?

Of the responses we received to our survey, two banks stood out as being those readers are most likely to recommend. Lunar was recommended by 35 percent people and Danske Bank by 27 percent.

The third-most recommended bank was Nordea, while several other banks got one or two recommendations.

Why were these banks singled out for recommendation?

For Lunar, the ease and speed of opening an account, app in English, and lack of a conversion fee for foreign currency were cited as benefits of using the bank.

“Easiest to open an account and get set up. Their app is great. I have found out that the process for other banks to be quite time consuming and cumbersome,” one reader wrote.

“Easy to use and fully English friendly,” said a French reader in Copenhagen.

While Lunar is a 100 percent digital bank, the legacy bank Danske Bank, the largest lender in Denmark, was praised for similar reasons.

“Simple process and helpful customer care manager” were features at Danske Bank, one reader from India, who works for a large company in Copenhagen, wrote to say.

An English-language version of Danske Bank’s app and mobile banking, and the bank’s general use of English, were also cited by several readers.

“They have English web interface and happy to communicate in English,” one wrote.

READ ALSO: REVEALED: Danish banks’ policies on non-Danish speaking customers

Another said Danske Bank was “More open to our situation - was completely thrown out by Nordea when wanting make an account 5 years ago and, more recently, when I wanted to buy a house Nordea offered us laughable rates as foreigners.”

“Danske treated us as equals to citizens,” they said.

Despite this negative review of Nordea, the pan-Nordic bank also had its share of recommendations.

Nordea has “less fees, good service in English” one of our readers said, with another adding that it offers “excellent app in English, great customer service and easy home loan process for non-Danish speakers”.

There was also some praise for smaller banks. For example, Lån & Spar is “much more flexible when issuing loans for property purchases and are willing to go fairly close to the 5 percent minimum for down payments, whereas big banks will flat out reject you if you have less than 20 percent saved,” wrote Nikola from Bulgaria, who lives in Copenhagen.

“Additionally, their advisors are very responsive and skilful at explaining the complex Danish mortgage system,” he added.

Which banks should you avoid according to readers?

“Danske Bank, unless you're a Russian oligarch and need to launder some money,” according to Nikola, presumably in reference to a major money laundering scandal at Danske Bank in the late 2010s.

READ ALSO: Money laundering scandal costs trust amongst Danske Bank customers

“While they do cater to foreign customers, they clearly have a preference to very wealthy ones and will happily ignore everyone else,” Nikola elaborated.

The number of readers who advised against using a specific bank was limited, but the two banks most frequently mentioned were Danske Bank and Nordea. Since these two banks were also highly recommended, this may reflect their size.

One reader wrote that Nordea “really do not care for you”, with another saying “I started with Nordea but merely got a Dankort debit [card], no MasterCard and no benefits that's why I changed.”

READ ALSO: Dankort: What is Denmark’s payment card and how is it different from other card types?

It’s best not to use “tier 1 banks as Danske or Nordea as the onboarding could be very long due to which expats will not receive the account in time,” according to one reader, who may have had in mind the requirement for Danish salaries to be paid into a Danish bank account under immigration laws.

In general, avoid “all of those that don't have dedicated full-service English based web services”, said another of the readers who responded to our survey.

Any other advice?

“For everyday banking, there's very little difference from one bank to the next. They all have low fees and offer the basics. For mortgages, it's valuable to shop around and play them one vs the other, especially if you're a higher earner. Banks do have some leeway when it comes to loan fees and they'll be willing to go lower if they want to capture you as a customer,” Nikola said.

When you go to open an account, “have the documents like CPR number, residence permit , employment contract, passport, address proof from home country [and] rental agreement,” one reader said.

“Check for fees and go to the physical bank to get a feeling on how much the staff is willing to help you before you open an account,” another said.

They added that “I could feel Jyske [bank] was bad but had just arrived here so couldn’t see the difference yet between being a Dane [reserved towards strangers, ed.] and being annoyed [about helping] foreigners”.

Join the conversation in our comments section below. Share your own views and experience and if you have a question or suggestion for our journalists then email us at [email protected].

Please keep comments civil, constructive and on topic – and make sure to read our terms of use before getting involved.

Please log in here to leave a comment.