The weakness of the pound could cause major financial headaches for some Brits in Denmark. Photo by Colin Watts on Unsplash

The value of the British pound has fallen steeply against the dollar in recent days but also against the Euro – and the krone. So what should you do if you live in Denmark but have income – such as a pension, rental income or a salary – in pound sterling?

Advertisement

Exchange rates might sound like a spectacularly dull topic, but if you live in Denmark (where, naturally, your day-to-day living expenses are paid in kroner) but have income from the UK in pounds, then the movement of the international currency markets will have a major impact on the money that ends up in your pocket.

This is not an uncommon situation – Denmark-based Brits may work remotely as freelancers from British companies and be paid for invoices in pounds, while retired Brits might be receiving a British pension.

Others might have income from rental properties or investments.

Advertisement

So a big loss in the value of the pound against the euro – and by extension, the krone – can have a major impact on Brits in Denmark.

The most recent fall in the value of the pound was sparked by the UK government’s new mini budget and has already seen a relative recovery.

The pound-krone exchange rate over the last month. Chart: xe.com

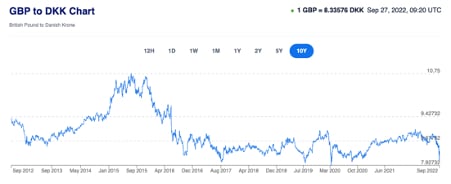

But while this one-time fall is spectacular, it’s also part of a longer term trend in the fall of the value of the pound, especially since Brexit, that has seen people such as foreign-based pensioners lose a big chunk of their income.

The pound-krone exchange rate over the last 10 years. Graph: xe.com

So if you have income in pounds, what are your options?

Income in kroner – obviously this isn’t an option for everyone, especially pensioners, but the best way to protect against currency exchange shocks is to make sure that you’re paid in the same currency that you spend in.

Alternatively, income in euros: the advantage of the euro in Denmark is that its value is pegged to the krone and not sensitive to exchange rate fluctuations.

For those being paid from abroad, billing in euros means you could work in any EU country – including the anglophone ones like Ireland – and get your salary in euros.

Depending on your employer, it might also be possible for you to ask to bill in euros.

Advertisement

Work in Denmark – if you’re currently not working or want to switch to local currency income, then an obvious option is to take up some work in Denmark.

Depending on your work and residency status, as well as the field you work, the practicality of this option ranges wildly from one person to the next.

Exchange rate – if your income can only be paid in pounds, it’s crucial to ensure that you get the best exchange rate possible and that you don’t waste money on international transfer fees.

The best options here are online banks or money transfer services, which compete on the rates that they offer, so usually have the most advantageous rate.

Some online banks also have the option to set up accounts in both pounds and kroner, so that you can receive money in pounds and spend it in kroner without having to make bank transfers, which can attract fees.

Join the conversation in our comments section below. Share your own views and experience and if you have a question or suggestion for our journalists then email us at [email protected].

Please keep comments civil, constructive and on topic – and make sure to read our terms of use before getting involved.

The pound-krone exchange rate over the last 10 years. Graph: xe.com

The pound-krone exchange rate over the last 10 years. Graph: xe.com

Join the conversation in our comments section below. Share your own views and experience and if you have a question or suggestion for our journalists then email us at [email protected].

Please keep comments civil, constructive and on topic – and make sure to read our terms of use before getting involved.

Please log in here to leave a comment.