job

For Members

Working in Denmark: Pension and insurance

The Local Denmark - [email protected]

Published: 24 Mar, 2015 CET.

Updated: Tue 24 Mar 2015 07:25 CET

Even in Denmark, where health insurance and pension are provided by the state, many companies offer private plans. Human resources expert Nancy Rasmussen tells you what you need to know about private pension and insurance options.

Editor's note: an updated version of this article can be found here.

One of the advantages of working for a company – as opposed to being self-employed – are the employee benefits. Many of the benefits, such as pension and insurance, are for the long-term and therefore easy to relegate to the back of your mind. But it’s worth it to take some time upfront to ensure that they are set up in a way that benefits you the most.

Many companies in Denmark offer pension and insurance coverage to their employees via a third-party provider, often the same provider for both. In the first month or so of your employment, you may be invited to a meeting with an advisor to help you make some decisions. I would strongly encourage you to prioritize this meeting. If for some reason you don’t automatically get an appointment, then I would suggest that you speak to your HR department or manager for guidance as there are some decisions you’ll need to make.

Pension

Pension

Remember that NemID that I mentioned a few weeks back? Well you’re going to need it. There is a site called PensionsInfo.dk which you can log into with NemID that has a full overview of all of your Danish pension accounts.

There are several kinds of pension included in this overview including:

State sponsored pension (Folkepension) – not related to your employment.

ATP (Arbejdsmarkedets Tillægspension) – a supplementary labour market pension scheme which nearly everyone in Denmark pays into. Deductions are automatically taken out of your paycheck, when which you can see on your pay slips.

Private pension - If your company offers a private pension programme, then you will also see line items on your pay slips for employer and employee contributions.

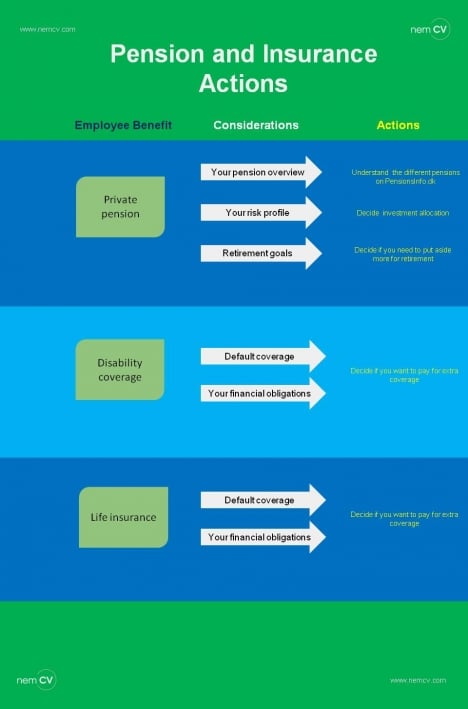

You and your advisor will discuss a bit about your personal and family situation and how comfortable you are with investment risk. Then you will sign-off on the investment allocation strategy. In general terms, you will pick what percentage of your pension contributions will be invested in equities (known for higher risk and higher return) versus bonds (lower risk, lower return).

If you think that you will leave Denmark before you retire, you should mention this to your pension advisor to discuss your options. You will generally be able to take the pension with you, but you will have to pay high taxes if you take the money before retirement age. I believe that there are some pension schemes for expats that can mitigate this, but this is something to discuss with the pension advisor.

Insurances

You may also be presented with a variety of insurance options. Some are included in your benefits package as-is and for others you will have some decisions to make.

Health Insurance – Many companies provide private health insurance, which you can use in addition to the state health insurance. This may also include seeing a chiropractor, psychologist, physical therapist, etc. It is a good idea to review what is covered before you actually ever need to use the insurance.

Disability insurance – This insurance is called loss of earning/occupational capacity. It protects you if lose the ability to work by continuing to pay you a percentage of your salary. Your benefit generally includes a default level of coverage and then you can pay extra if you want to a higher level of coverage. It is especially important to review your coverage level if you have for example a mortgage, kids, or other serious financial obligations.

Life Insurance – This benefit provides an amount to your beneficiary should you pass away while employed. You should review the amount of this coverage to make sure that your survivors will be amply covered. It’s not fun to think about, but it’s very important to get this right before anything unexpected happens.

Critical Illness - This is often included in your benefits package and it’s basically a payment to you in the event that you become critically ill. Your provider will have a list of what illnesses count as critical. You can generally use the money however you wish, as it’s meant to ease the burden of dealing with a serious illness.

At the end of your meeting, you’ll get an overview of everything you’ve decided on and you should keep a copy for your records. The information is usually also available if you log into your provider’s website.

Do you find this information to be helpful? What do you want to learn more about? Let us know!

Nancy Rasmussen is currently employed as a Change Management Consultant, supporting IT projects. She has more than 12 years of experience within large, international companies. She writes this column in her free-time in connection with NemCV. This column is not affiliated with her current full-time employment.

Nancy Rasmussen is currently employed as a Change Management Consultant, supporting IT projects. She has more than 12 years of experience within large, international companies. She writes this column in her free-time in connection with NemCV. This column is not affiliated with her current full-time employment.

Comments

See Also

Editor's note: an updated version of this article can be found here.

One of the advantages of working for a company – as opposed to being self-employed – are the employee benefits. Many of the benefits, such as pension and insurance, are for the long-term and therefore easy to relegate to the back of your mind. But it’s worth it to take some time upfront to ensure that they are set up in a way that benefits you the most.

Many companies in Denmark offer pension and insurance coverage to their employees via a third-party provider, often the same provider for both. In the first month or so of your employment, you may be invited to a meeting with an advisor to help you make some decisions. I would strongly encourage you to prioritize this meeting. If for some reason you don’t automatically get an appointment, then I would suggest that you speak to your HR department or manager for guidance as there are some decisions you’ll need to make.

Pension

Remember that NemID that I mentioned a few weeks back? Well you’re going to need it. There is a site called PensionsInfo.dk which you can log into with NemID that has a full overview of all of your Danish pension accounts.

Remember that NemID that I mentioned a few weeks back? Well you’re going to need it. There is a site called PensionsInfo.dk which you can log into with NemID that has a full overview of all of your Danish pension accounts.

There are several kinds of pension included in this overview including:

State sponsored pension (Folkepension) – not related to your employment.

ATP (Arbejdsmarkedets Tillægspension) – a supplementary labour market pension scheme which nearly everyone in Denmark pays into. Deductions are automatically taken out of your paycheck, when which you can see on your pay slips.

Private pension - If your company offers a private pension programme, then you will also see line items on your pay slips for employer and employee contributions.

You and your advisor will discuss a bit about your personal and family situation and how comfortable you are with investment risk. Then you will sign-off on the investment allocation strategy. In general terms, you will pick what percentage of your pension contributions will be invested in equities (known for higher risk and higher return) versus bonds (lower risk, lower return).

If you think that you will leave Denmark before you retire, you should mention this to your pension advisor to discuss your options. You will generally be able to take the pension with you, but you will have to pay high taxes if you take the money before retirement age. I believe that there are some pension schemes for expats that can mitigate this, but this is something to discuss with the pension advisor.

Insurances

You may also be presented with a variety of insurance options. Some are included in your benefits package as-is and for others you will have some decisions to make.

Health Insurance – Many companies provide private health insurance, which you can use in addition to the state health insurance. This may also include seeing a chiropractor, psychologist, physical therapist, etc. It is a good idea to review what is covered before you actually ever need to use the insurance.

Disability insurance – This insurance is called loss of earning/occupational capacity. It protects you if lose the ability to work by continuing to pay you a percentage of your salary. Your benefit generally includes a default level of coverage and then you can pay extra if you want to a higher level of coverage. It is especially important to review your coverage level if you have for example a mortgage, kids, or other serious financial obligations.

Life Insurance – This benefit provides an amount to your beneficiary should you pass away while employed. You should review the amount of this coverage to make sure that your survivors will be amply covered. It’s not fun to think about, but it’s very important to get this right before anything unexpected happens.

Critical Illness - This is often included in your benefits package and it’s basically a payment to you in the event that you become critically ill. Your provider will have a list of what illnesses count as critical. You can generally use the money however you wish, as it’s meant to ease the burden of dealing with a serious illness.

At the end of your meeting, you’ll get an overview of everything you’ve decided on and you should keep a copy for your records. The information is usually also available if you log into your provider’s website.

Do you find this information to be helpful? What do you want to learn more about? Let us know!

Nancy Rasmussen is currently employed as a Change Management Consultant, supporting IT projects. She has more than 12 years of experience within large, international companies. She writes this column in her free-time in connection with NemCV. This column is not affiliated with her current full-time employment.

Join the conversation in our comments section below. Share your own views and experience and if you have a question or suggestion for our journalists then email us at [email protected].

Please keep comments civil, constructive and on topic – and make sure to read our terms of use before getting involved.

Please log in here to leave a comment.